AEP: Anglo-Eastern Plantations – A Potential Long Position

In case my latest diary entry doesn’t quite portray it, I am very new to the world of investing. So much so, that I have no doubt this analysis will be cross-referenced, disputed, laughed at or even bollocked for all it’s shortcomings. Nonetheless, I think it’s important to introduce with that disclaimer, so you’re all aware of the level of ‘insight’ you’ll read below.

My investment strategy is, well, in it’s infancy. In fact, it’s not even a strategy. I am in the process of poring over information from a screen set up in Stockopedia. There’s roughly a dozen companies that have met my criteria to find under-valued companies and it’s my job to look over the key financial data and work out whether I see a genuine diamond in the rough, or a company on the verge of a huge boost in share price.

Talk to the Palm

One of the first companies that caught my eye, was Anglo-Eastern Plantations (AEP). It first and foremost stood out to me from it’s performance over the last twelve months. At the time of writing this, from October the 7th 2024, to today’s price, it has double in value from 650.00p to 1350.00p. It is by far one of the most appealing from the list of companies on my screen on this metric alone.

So who are they? Well, trying my hardest not to copy and paste their profile summary from Stockopedia, AEP is a company that is like a big farmer based in the UK that runs huge fields, mostly in Indonesia and Malaysia, to grow and harvest things like palm oil and rubber.

As a newcomer to this investment game, I certainly understand what AEP do from reading their company background, but I need some fulfilment in understanding what it is that makes them so lucrative (over the last year or so anyways) and whether or not it’s a safe haven for continued investment growth.

Let’s Talk Numbers

An interesting metric which I learned from The Naked Trader (it’s a book, not some questionable superhero) was to look at companies where the current market capitalisation, does not exceed 15 times the net profit of the company. This is described as a method to spot an undervalued company and described in the book as part of the ‘billionaire test’.

From doing a bit more research on this, it turns out this is a metric known as the P/E Ratio or ‘Price to Earnings Ratio’. Taking the current market capitalisation and dividing by the latest net profit figures (or estimated profits, if available). A general rule-of-thumb has always been to aim to get this figure at 15 or so.

Going back to AEP’s financials then, their P/E ratio (or billionaire test) sits nicely at 8.21, following their interim report in August 2025, covering the period up to the 30th of June 2025. Let’s delve further.

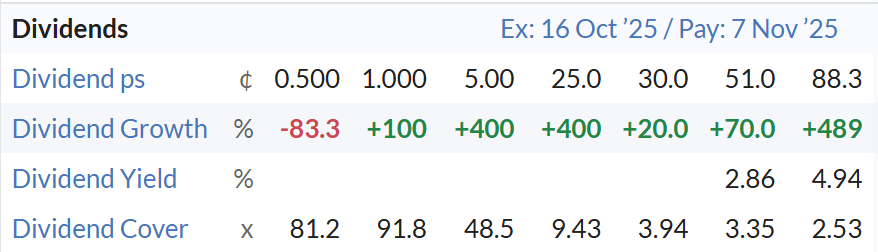

One thing I now want to see, is dividend growth. More importantly, a consistent growth year-on-year. This indicates that only the company is secure and on-top of any wasteful spending. More importantly, there is a healthy cash reserve within the business. Looking at the year-on-year figures for dividends per share, I can see a a very solid growth indeed.

Looking then at debt, and it’s another huge positive for AEP. The company has no bank borrowings and reports a negative net-debt position of $-262m for the last 12 months and has done since at least 2020. This gives AEP a very healthy outlook indeed, holding cash reserves of circa $245m, an increase of roughly $63m from year-end results in 2024.

Certainly reading from the financials, all boxes appear to be ticked. Steadily rising revenues and net profits to match. Strong dividend growth year-on-year and an extremely healthy cash reserve, with no debt.

We’ll Have it Back

Reading through the latest interim report, it does seem as though the company has thoughts around under-valuation. So much so, they have announced share buybacks. Simply put, the company feels the company is undervalued by their own metrics and is buying $8m of the available shares on the market. This tell me two things. One being that the company is confident of having the spare cash to use on buying the shares back, without jeopardising future growth. The other, is that reducing the amount of shares on the market, the Earnings per Share (EPS) will grow. This also makes the ‘billionaire test’ more appealing, assuming net profits remain on a good trajectory.

So what’s stopping the further growth?

Well, reading through the report, it does seem a major contributor to their growth is the price of palm oil. Since last year, the price of palm oil increased by 15%. There could be a lot of factors that stop that trajectory. If the demand for bio-diesel wanes, or there’s a poor view around deforestation, then it may well take a decline.

However.

From what I read around the Indonesian government, there are mandates about it’s use for bio-diesel, which requires palm oil. Currently, the country operates what’s known as the B40 policy. This requires all diesel to have a 40% blend of palm oil. There are now aims for this to be 50% by 2026, with the B50 mandate. But this is only achievable through levies it places on the export of palm oil. The government’s ambition for B50 by 2026 signals guaranteed future demand for palm oil, which is a positive for AEP’s revenues. However, the reliance on export levies to fund the exponentially increasing subsidy cost creates a significant risk of profit margins for AEP, as the government will likely raise the tax it imposes on AEP’s profitable export sales.

Summary

I really can’t see past this stock at the moment. I’m trying my best to not veer into confirmation bias on what I’ve read and the healthy balance sheet. There are some risks attached to the stock. If there is less demand globally for palm oil, this may hurt profits going forward. But locally, the demand seems ever increasing. Providing the demand and crucially, the price for palm oil remains high, then AEP seems to have good short to medium growth. They have also invested in an 8th mill, which is likely to be commissioned in December 2026. So the appetite for growth is certainly evident.

So how will I play it? This is where my basic chart analysis comes into play. I can see from the daily chart, support is bouncing around 1315.00p, so I’ll look for this as my entry point, or around 1320.00p. A stop-loss will likely go in 1118.00p, to keep any losses at around 15% and trail it by 15% if and when it moves up. In terms of an exit price, it’s tough. I think 1700.00p is possible, but that’s entirely speculation at this point. The next annual report is due at the end of the year, so I’ll wait and see how the market reacts first.